NCERT Solutions for Class 12 Accounts Part 2 Chapter 4: Analysis of Financial Statements

NCERT Solutions for Class 12 Accounts Part 2 Chapter 4 Analysis of Financial Statements explains in detail how the financial statement of a company is read and analyzed so as to derive the financial health of the company. This chapter discusses basically the various techniques and tools for financial analysis. It covers comparative statements, common-size statements, and trend analysis. The stepwise representation of the methods in the NCERT Class 12 Financial Statement Analysis Solutions words out the approach, providing insight into the application of the methods in the real world financial data.

Download PDF For NCERT Solutions for Accountancy Analysis of Financial Statements

The NCERT Solutions for Class 12 Accounts Part 2 Chapter 4: Analysis of Financial Statements are tailored to help the students master the concepts that are key to success in their classrooms. The solutions given in the PDF are developed by experts and correlate with the CBSE syllabus of 2023-2024. These solutions provide thorough explanations with a step-by-step approach to solving problems. Students can easily get a hold of the subject and learn the basics with a deeper understanding. Additionally, they can practice better, be confident, and perform well in their examinations with the support of this PDF.

Download PDF

Access Answers to NCERT Solutions for Class 12 Accounts Part 2 Chapter 4: Analysis of Financial Statements

Students can access the NCERT Solutions for Class 12 Accounts Part 2 Chapter 4: Analysis of Financial Statements. Curated by experts according to the CBSE syllabus for 2023–2024, these step-by-step solutions make Accountancy much easier to understand and learn for the students. These solutions can be used in practice by students to attain skills in solving problems, reinforce important learning objectives, and be well-prepared for tests.

TEST YOUR UNDERSTANDING I

Fill in the blanks with appropriate word(s).

Question 1. Analysis simply means———data.

Question 2. Interpretation means————-data.

Question 3. Comparative analysis is also known as—————Analysis.

Question 4. Common size analysis is also known as————–Analysis

Question 5. The analysis of actual movement of money inflow and outflow in an organization is called———-analysis.

1. Simplification .

2. Explaining

3. Horizontal

4. Vertical

5. cash flow

DO IT YOURSELF I

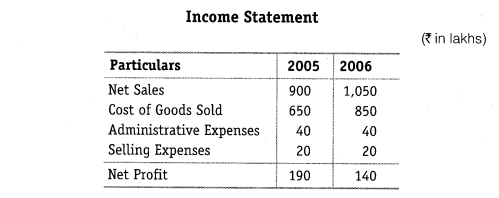

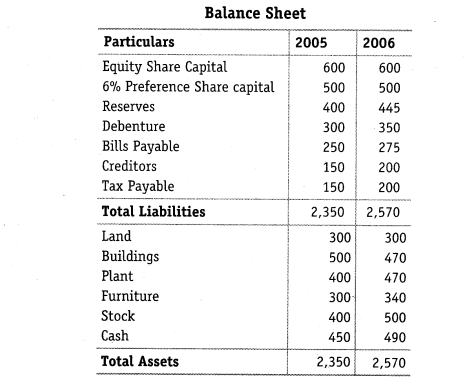

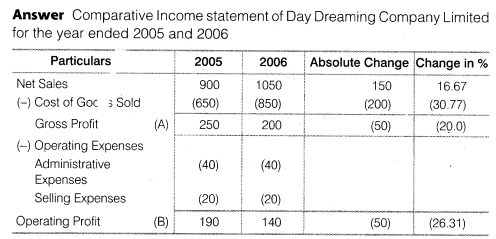

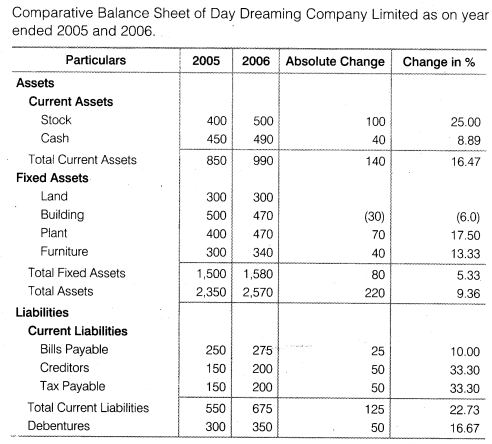

From the following balance sheet and income statement of Day Dreaming Co.Ltd., for the year ending 2002 and 2003, prepare the comparative statements.

DO IT YOURSELF II

The following are the Balance Sheets of Harsha Ltd. as on March 31, 2006 and March 31, 2007

TEST YOUR UNDERSTANDING – II

Choose the right answer :

1. The financial statements of a business enterprise include:

(a) Balance sheet

(b) Profit and loss account

(c) Cash flow statement

(d) All the above

2. The most commonly used tools for financial analysis are:

(a) Horizontal analysis

(b) Vertical analysis

(c) Ratio analysis

(d) All the above

3. An Annual Report is issued by a company to its:

(a) Directors

(b) Auditors

(c) Shareholders

(d) Management

4. Balance Sheet provides information about financial position of the enterprise:

(a) At a point in time

(b) Over a period of time

(c) For a period of time

(d) None of the above

5. Comparative statement are also known as:

(a) Dynamic analysis

(b) Horizontal analysis

(c) Vertical analysis

(d) External analysis

1. (d) All of above

2. (d) All of above

3. (c) Shareholders

4. (a) At a Point of time

5. (b) Horizontal analysis

DO IT YOURSELF III

The following data is available from the P&L Account of Deepak Limited

TEST YOUR UNDERSTANDING III

(a) The financial statements of a business enterprise include funds flow statement.

(b) Comparative statements are the form of horizontal analysis.

Answer True

(c) Common size statements and financial ratios are the two tools employed in vertical analysis.

(d) Ratio analysis establishes a relationship between two financial statements.

Answer False

(e) Ratio analysis is a total for analysing the financial statements of any enterprise.

(f) Financial analysis is used only by the creditors.

(g) Profit and loss account shows the operating performance of an enterprise for a period of time.

(h) Financial analysis helps an analyst to arrive at a decision.

(i) Cash flow statement is a tool of financial statement analysis.

(j) In a common size statement each item is expressed as a percentage of some common base.

(a) False

(b) True

(c) True

(d) False

(e) True

(f) False

(g) True

(h) True

(i) True

(j) True

SHORT ANSWER TYPE QUESTIONS

Explain the meaning of Analysis and Interpretation.

Analysis and Interpretation refers to a systematic and critical examination of the financial statements. It not only establishes cause and effect relationship among the various items of the financial statements but also presents the financial data in a proper manner.

The main purpose of Analysis and Interpretation is to present the financial data in such a manner that is easily understandable and self explanatory. This not only helps the accounting users to assess the financial performance of the business over a period of time but also enables them in decision making and policy and financial designing process.

List the techniques of Financial Statement Analysis.

The following are the commonly used techniques of Financial Statement analysis

(i) Ratio Analysis (li) Cash Flow Statement

(iii) Fund Flow Statement

(iv) Comparative Financial Statements

(v) Common Size Financial Statements

(vi) Trend Analysis

Bring out the importance of Financial Analysis.

Financial Analysis has great importance to various accounting US’ on various matters. Income Statements, Balance Sheets and other financ data that provides information about expenses and sources of income, profi loss and also helps in assessing the financial position of a business. The financial data are not useful until they are analysed. There are various tools a methods such as Ratio Analysis, Cash Flow Statements that make the financ data to cater varying needs of various accounting users.

The following are the reasons that advocate in favour of Financial Analys

(i) It helps in evaluating the profit earning capacity and financ feasibility of a business.

(ii) It helps in assessing the long-term solvency of the business.

(iii) It helps in evaluating the relative financial status of a firm comparison to other competitive firms.

(iv) It assists management in decision making process, plans and also in establishing an effective controlling

What are Comparative Financial Statements?

Those financial statements that enable intra-firm and comparisons of financial statements over a period of time are called Comparative Financial Statements. In other words, these statements help the accounting users to evaluate and assess the financial progress in the relative terms.

These statements express the absolute figures, absolute change and the percentage change in the financial items over a period of time. Comparative Financial Statements present the financial data in such a manner that is easily understandable and can be analysed without any ambiguity. If the accounting policies and practices for the treatment of the items are the same over the period of study, only then the Comparative Financial Statements enable meaningful comparisons.

The following are the two Comparative Financial Statements that are commonly prepared

(i) Comparative Balance Sheet

(ii) Comparative Income Statements

What do you mean by Common Size Statements?

These statements depict the relationship between various items of financial statements and some common items (like Net Sales and the Total of Balance Sheet) in percentage terms. In other words, various items of Trading and Profit and Loss Account such as Cost of Goods Sold, Non-Operating Incomes and Expenses are expressed in terms of percentage of Net Sales.

On the other hand, different items of Balance Sheet such as Fixed Assets, Current Assets, Share Capital etc are expressed in terms of percentage of Total of Balance Sheet. These percentage figures are easily comparable with that of the previous years’ and with that of the figures of other firms in the same industry {i.e., inter-firm comparison) as well.

The analyses based on these statements are commonly known as Vertical Analysis.

The following are commonly prepared Common Size Statements.

(i) Common Size Balance Sheet

(ii) Common Size Income Statements

LONG ANSWER TYPE QUESTIONS

Describe the different techniques of financial analysis and explain the limitations of financial analysis.

The most commonly used techniques of financial analysis are as follows

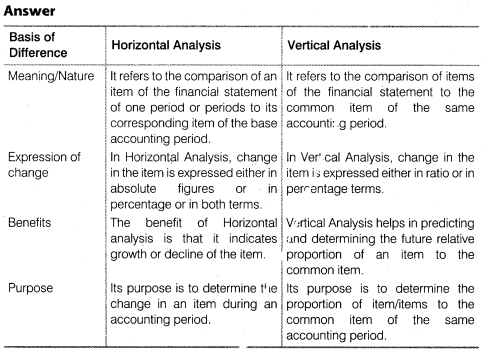

(i) Comparative Statements: These are the statements showing the profitability and financial position of a firm for different periods of time in a comparative form to give an idea about the position of two or more periods. The financial data will be comparative only when same accounting principles are used in preparing these statements. Comparative figures indicate the trend and direction of financial position and operating results. This analysis is also known as ‘horizontal analysis’.

(ii) Common Size Statements: These are the statements which indicate the relationship of different items of a financial statement with some common item by expressing each item as a percentage of the common item. The percentage thus calculated can be easily compared with the results corresponding percentages of the previous year or of some other firms, as the numbers are brought to common base. Such statements also allow an analyst to compare the operating and financing characteristics of two companies of different sizes in the same industry. This analysis is also known as ‘Vertical analysis’.

(iii) Trend Analysis :It is a technique of studying the operational results and financial position over a series of years. Using the previous years’ data of a business enterprise, trend analysis can be done to observe the percentage changes over time in the selected data. Trend analysis is important because, with its long run view, it may point to basic changes in the nature of the business. By looking at a trend in a particular ratio, one may find whether the ratio is falling, rising or remaining relatively constant. From this observation, a problem is detected or the sign of good management is found. .

(iv) Ratio Analysis :It describes the significant relationship which exists between various items of a balance sheet and a profit and loss account of a firm. As a technique of financial analysis, accounting ratios measure the comparative significance of the individual items of the income and position statements.

(v) Cash Flow Analysis :It refers to the analysis of actual movement of cash into and out of an organisation. The flow of cash into the business is called as cash inflow or positive cash flow and the flow of cash out of the firm is called as cash outflow or a negative cash flow. The difference between the inflow and outflow of cash is the net cash flow.

Limitations of Financial Analysis

The following are the limitations of Financial Analysis

(i) Ignorance of Price Level Changes :Financial statement is based on historical cost method and fails to capture the change in price level. The figures of different years are taken on nominal values and not in real terms (i.e., not taking price change into considerations).

(ii) Misleading and Wrong information: The financial analysis fails to reveal the change in the accounting procedures and practices. Consequently, they may provide wrong and misleading information.

(iii) Fail to Provide Final Picture: The financial analysis presents only the interim report and thereby provides incomplete information. They fail to provide the final and holistic picture.

(iv) Consider Only Monetary Aspect: This is one of the limitations of financial analysis that it reveals only the monetary aspects. Only those items are considered here which can be measured in term of money and fail to disclose managerial efficiency, growth prospects, and other non-operational efficiency of a business.

(v) Non-Reliable Conclusions :Conclusion base on financial analysis may be non reliable because financial statement are based on certain concepts and conventions.

(vi) Involves Personal Biasness: The financial analysis reflects the personal biasness and personal value judgments of the accountants and clerks involved. There are different techniques used by different personnel for charging depreciation (original cost or written-down value method) and also for inventory valuation. The use of different techniques by different people reduces the effectiveness of the financial analysis.

(vii) Unsuitable for Comparisons :Due to the involvement of personal value judgment, personal biasness and use of different techniques by different accountant, various types of comparisons such as inter-firm and intra-firm comparisons may not be possible and reliable.

Explain the usefulness of trend percentages in interpretation of financial performance of a company.

The Trend Analysis presents each financial item in percentage terms for each year. These Trend Analysis not only help the accounting users to assess the financial performance of the business but also assist them to form an opinion about various tendencies and predict the future trend of the business.

Usefulness and Importance of Trend Analysis:

The following are the various importance of Trend Analysis

(i) Assists in Forecasting: The trends provided by Trend Analysis help the accounting users to forecast the future trend of the business.

(ii) Percentage Terms: The trends are expressed in percentage terms. Analysing the percentage figures is easy and also less time consuming.

(iii) User Friendly: As the trends are expressed in percentage figures, so it is the most popular financial analysis to analyse the financial performance and operational efficiency of the company. In other words, one needs not to have an in-depth and sophisticated knowledge of accounting in order to analyse these percentage trends.

(iv) Presents a Broader Picture :The trend analysis presents a broader picture about the financial performance, viability and operational efficiency of a business. Generally, companies prefer to present their financial data for a period of 5 or 10 years in forms of percentage trends.

What is the importance of comparative statements? Illustrate your answer with particular reference to comparative income statement.

The following are the importance of Comparative Statements.

(i) Make Presentation Simpler : Comparative statements presents the financial data in a simpler form. On the other hand, an year-wise data of the same items are presented side-by-side, which not only makes the presentation clear but also enables easy comparisons (both intra-firm and inter-firm) conclusive.

(ii) Help in Drawing Conclusion: The presentation of comparative statement is so effective that it helps the analyst to draw conclusion quickly and easily and that too without any ambiguity.

(iii) Help in Forecasting :The management may analyse the trend and forecast and draft various future plans and policy measures, with the help of comparative statement:

(iv) Help in Detection of Problems :The comparative analysis not only enables the management in locating the problems but also helps them to put various budgetary controls and corrective measures to check whether the current performance is aligned with that of the ” planned targets. With the help of the comparison of the financial data of two or more years, the financial management can easily detect the problems.

What do you understand by analysis and interpretation of financial statements? Discuss their importance.

Financial Analysis has great importance to various accounting users on various matters. Income Statements, Balance Sheets and other financial data‘provide information about expenses and sources of income, profit or loss and also helps in assessing the financial position of a business.

These financial data are not useful until they are analysed. There are various tools and methods such as Ratio Analysis, Cash Flow Statements that make the financial data to cater varying needs of various accounting users.

The following are the reasons that advocate in favour of Financial Analysis

(i) It helps in evaluating the profit earning capacity and financial feasibility of a business.

(ii) It helps in assessing the long-term solvency of the business.

(iii) It helps in evaluating the relative financial status of a firm in comparison to other competitive firms.

(iv) It assists management in decision making process, drafting various plans and also in establishing an effective controlling system.

Explain how common size statements are prepared giving an example.

Common size statements can be classified into two broad categories

(i) Common Size Income Statements

(ii) Common Size Balance Sheet

Common Size Statement is prepared in a columnar form for analysis. In a Common Size Statement, each item of the financial statements is compared to a common item. The analyses based on these statements are commonly known as Vertical Analysis.

The following are the columns prepared in a Common Size Statement

(a) Particulars Column:This column shows the various financial items under their respective heads.

(b) Amount Columns :These columns depict the amount of each item, sub-totals and the gross total of a particular year.

(c) Percentage or Ratio Columns :These columns show the proportion of each item to the common item either in terms of percentage or ratio.

The Common Size Statements can be presented in the following two ways.

Method 1 Percentage column is shown beside the amount column of the year to which percentage column belongs.

Method 2 Amount columns are shown first and their percentage columns are shown after the amount columns.

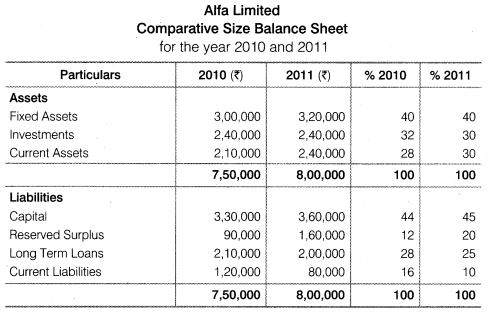

Example :From the following information provided by Alfa Limited Prepare the Common Size Statements.

NUMERICAL QUESTIONS

From the following information of Narsimham Company Ltd., prepare a Comparative Income Statement for the years 2004-2005

Interpretation

(i) The Net Profit of the company increased.

(ii) Simultaneously the company has tried to reduce its costs to improve its profit margin.

(iii) Profitability of the company has improved over the year.

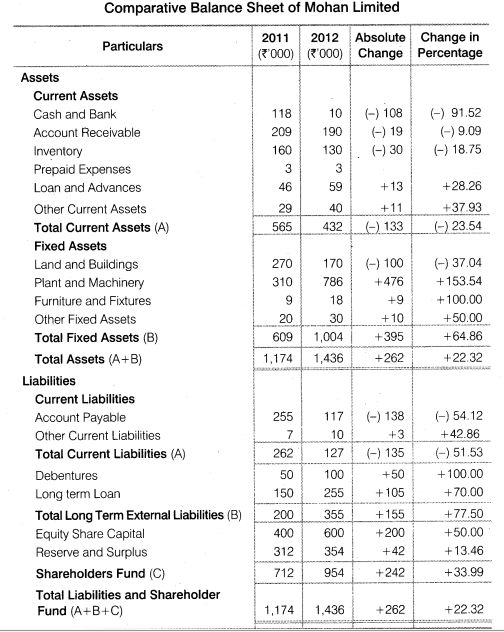

The following are the Balance Sheets of Mohan Ltd., at the end of 2004 and 2005.

Prepare a Comparative Balance Sheet and study the financial position of the company.

Comments

(i) Decrease in current Liabilities is more than decrease in current assets which indicates that the current ratio has improved.

(ii) Decrease in cash and bank may result in delay in payments.

(iii) Fixed Assets have increased along with share capital. It indicates that such asset has been purchased using Long term sources of finance.

(iv) Increase in reserve and surplus is a healthy indicator.

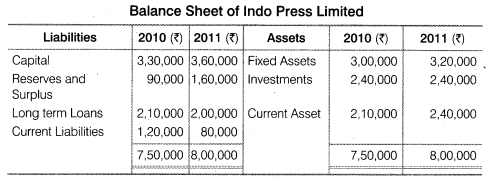

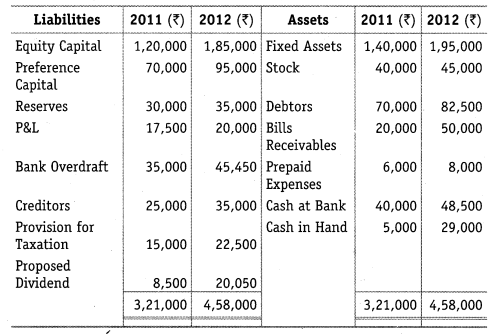

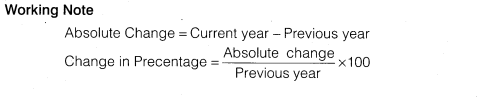

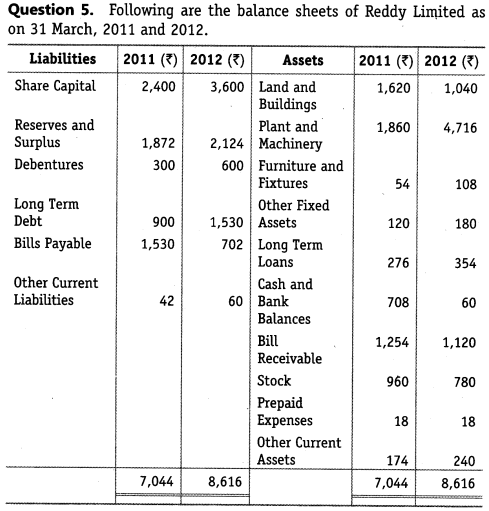

The following are the balance sheets of Devi Company Limited at the end of 2011 and 2012. Prepare a comparative Balance Sheet and study the financial position of the concern.

Comments

(i) Change in current assets and current Liabilities is almost same. It indicates that ratio is same as of previous year.

(ii) Fixed Assets have increased along with share capital which shows that assets are purchased with long term sources of finance.

(iii) The overall financial position of company is satisfactory.

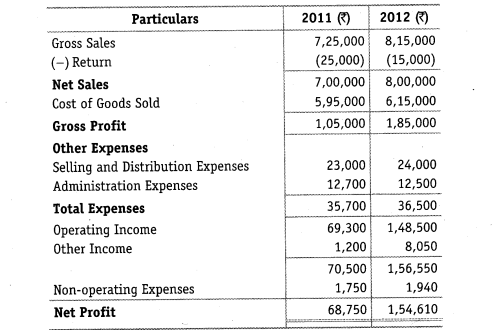

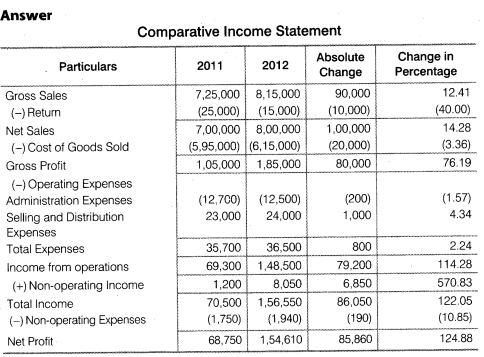

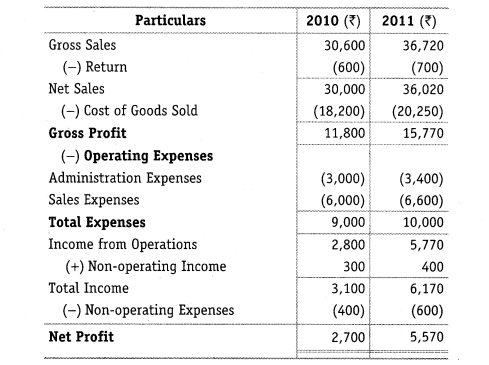

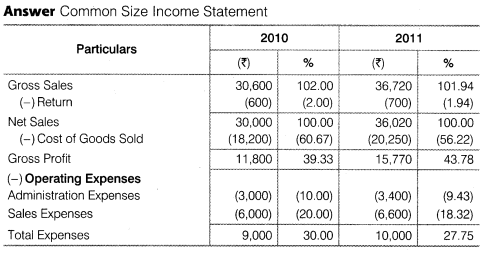

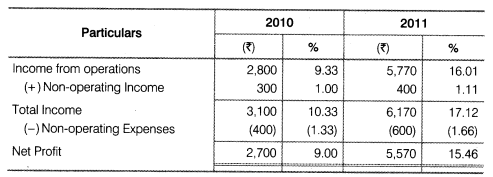

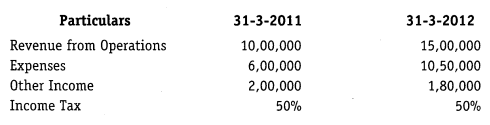

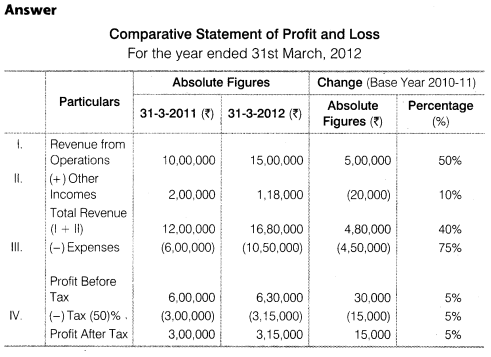

Convert the following Income Statement into Common Size Statement and interpret the changes in 2011 in the light of the conditions in 2010.

Comment: Company has reduced its cost and expenses which has resulted in increase in income from operations and net profit.

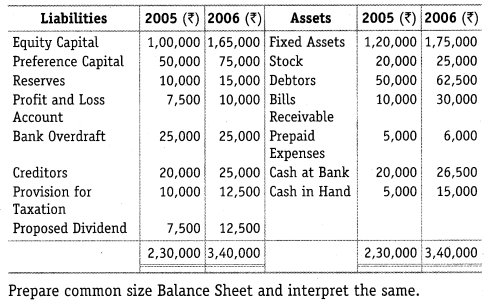

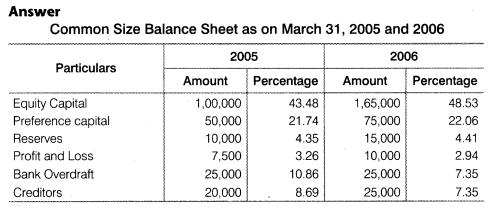

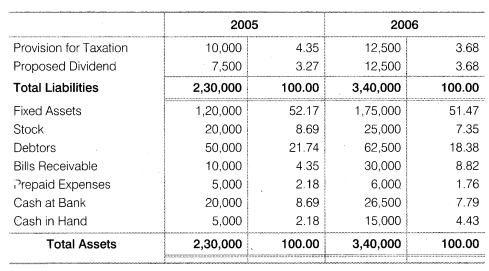

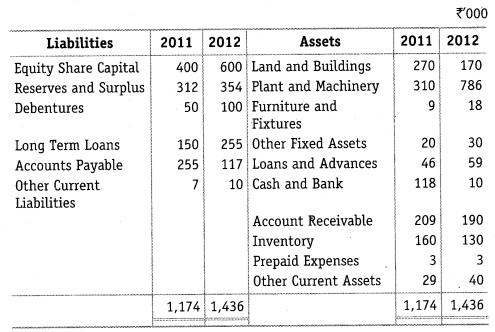

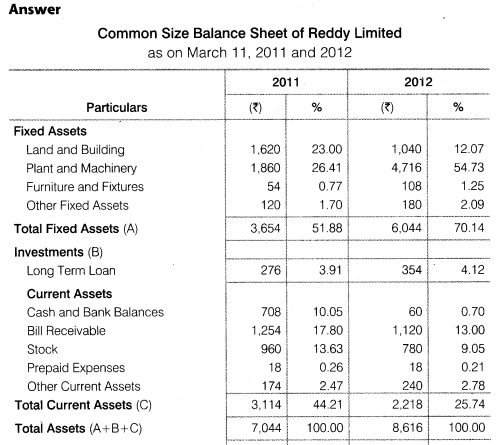

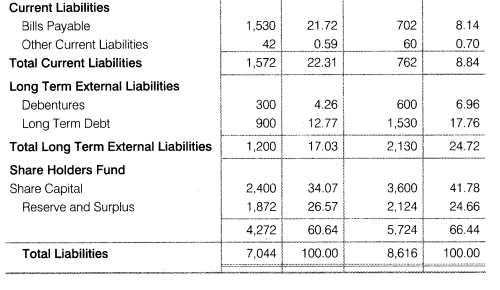

Analyse the financial position of the company with the help of the Common Size Balance Sheet.

Comments

(i) Inspite of decrease in current assets and current liabilities, the current ratio has improved.

(ii) Decrease in cash and bank balance indicates that there will be delay in payments.

(iii) Increase in fixed assets and share capital shows that assets are purchased with long term sources of finance.

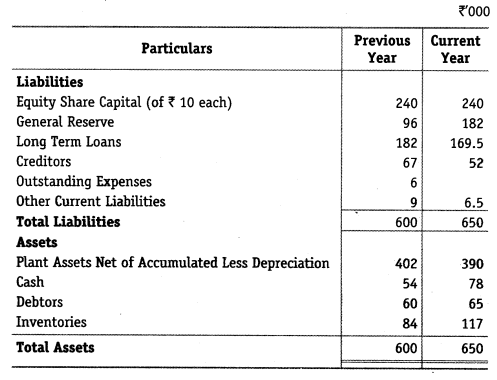

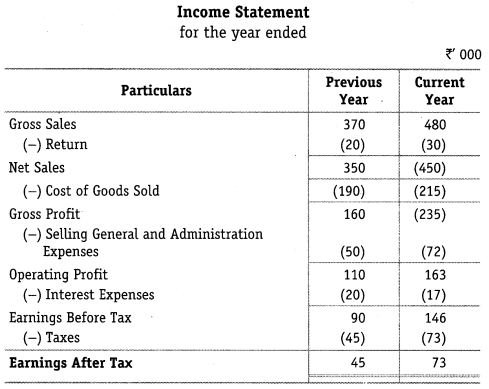

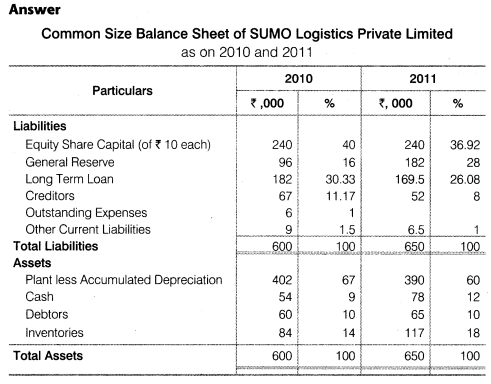

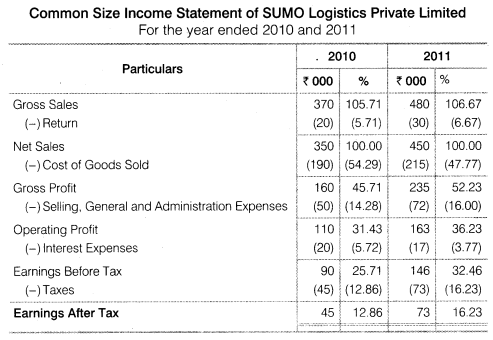

The accompanying balance sheet and profit and loss account related to SUMO Logistics Private Limited. Convert these into Common Size Statements.

Previous Year = 2010, Current Year = 2011

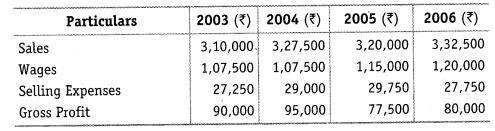

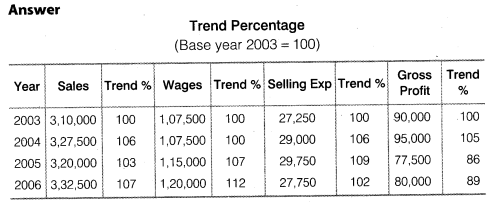

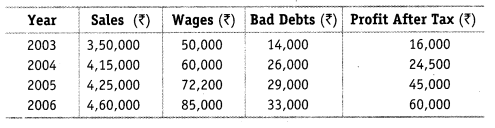

From the following particulars extracted from P&L Account of ‘Prashanth Limited, you are required to calculate trend percentages

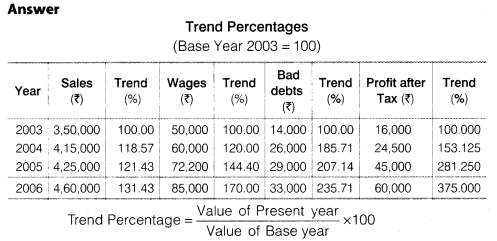

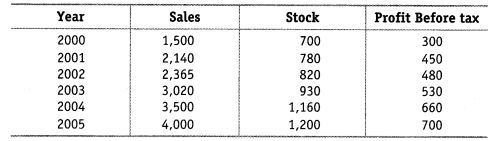

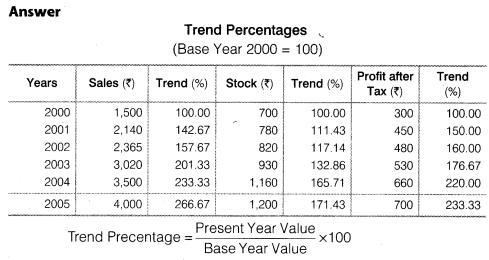

Calculate trend percentages from the following figures of ABC Limited, taking 2000 as base and interpret them.

Interpretations

(i) Sales has exhibited continuous increasing trend over the period.

(ii) The value of stock also increases, with the increase in value of sales.

(iii) Profit increase more in earlier years as compare to later years. It implies cost of goods, sold and operating expenses are increased in later years.

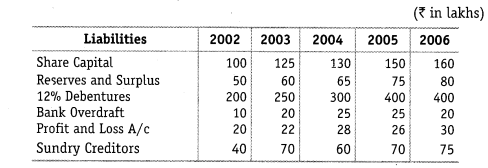

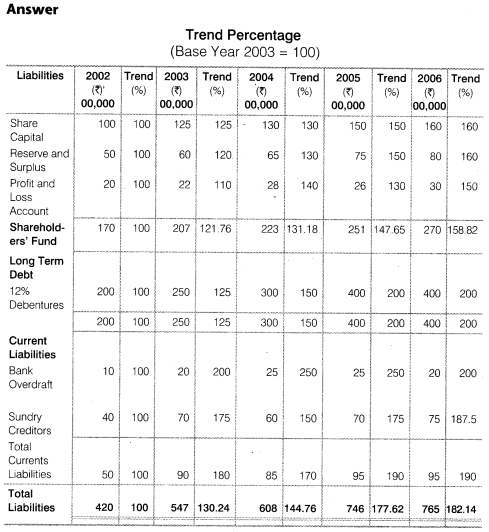

From the following data relating to the liabilities side of balance sheet of Madhuri Limited, as on 31st March, 2006, you are required to calculate trend percentages taking 2002 as the base year.

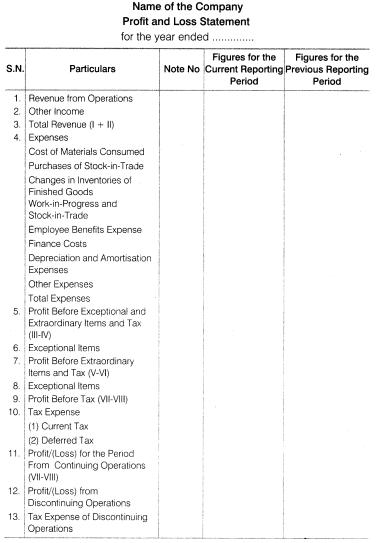

Effects of Revised Schedule VI on Tools of Analysis of Financial Statements As per revised Schedule VI part II the Format of Profit of Loss Statement is as follows.

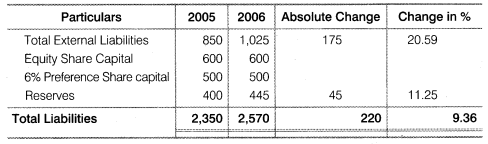

Prepare comparitive statements from the following.

Admissions Open for 2025-26